1.2 What Type of Business Risk Insurance You Should Have?

There are a variety of insurance choices available to business owners. Insurance protects your business from various circumstances that may occur during normal operations. Generally, business insurance can be classified into five main categories:

(a) Property Insurance:

To cover against losses to your property such as building and contents including inventories (stock-in-trade), furniture, equipment, plant & machinery. The most important property insurance is fire insurance which the coverage could also be extended to include special perils such as storm and tempest, flood, earthquake etc. Some other property insurances are burglary insurance, money insurance and plate glass insurance.

(b) Liability Insurance

To cover any damages and legal fees incurred as a result of negligence or breach of duty. Liability insurance policy includes public liability insurance, product liability insurance, professional indemnity insurance, employers’ liability insurance and workmen’s compensation insurance.

(c) Employee Insurance

To protect your employees against unexpected costly expenses due to accidents, critical illnesses and hospitalization. Employees are the greatest assets to almost any business. As an employer, you must give them the protection they deserve. You can choose to cover for group medical plan, group personal accident or group term life depending on the needs and suitability.

(d) Engineering Insurance

To cushion your projects and equipment against unexpected industrial incidents. Engineering insurance refers to the insurance that protects the ongoing construction project, installation project, and machines and equipment in project operation from financial loss.

(e) Marine Insurance

To covers the loss or damage of ships, cargo, terminals, and any transport or cargo by which property is transferred, acquired, or held between the points of origin and final destination.

One of the ways to determine what type of business insurance that you need is to learn what coverage suits you best depending on your business industry, size, location and number of employees. At minimum, you may want to at least purchase property and liability coverage. Other type of business insurance also exists, i.e insurance to cover your credit risks. Read below to read more on this trade credit insurance.

Business insurance should be review regularly, especially when your business grows, where your required coverage might change. Choosing the right business insurance might be difficult, but we're here to help.

Source: https://piam.org.my/

1.2.1 Risk With Your Receivables: Trade Credit Insurance

Most corporate client are feeling the economic consequences of Covid-19. During this challenging time, sellers are worried as their buyers / customers no longer able to pay on time. Many companies are seeking more information to have its protection to get through these difficult and challenging days that the COVID-19 is affecting national and international trade. – Trade Credit Insurance.

What is Trade Credit Insurance?

A protection that covers for business-to-business against the risk of non-payment from their corporate buyer. It’s covers both export and domestic credit sales.

Why Trade Credit Insurance?

Trade credit insurance is one of the key tools for your corporate risk management. It assured of the support on cashflow and liquidity. The benefits are:

i. Improve financing

ii. Enhanced credit management

iii. Balance sheet protection

iv. Independent assessment of new & existing buyer

v. Allowable tax deduction expenses; and

vi. Provide collection services.

Trade credit insurers are currently reviewing their exposures and will likely limit coverage amid the growing economic fallout from the coronavirus outbreak while experts urged businesses to shift from planning and preparation to proactively manage the impact of COVID-19 on their operations and employees.

As supply chain disruptions continue amid coronavirus lockdowns and quarantines, many business bankruptcies are expected to increase. As they are aware of many companies that are trading into some of the red zone areas too, credit insurers are currently reviewing their exposures and are expecting losses to increase over the coming weeks and months.

At this current economy downturn, all the credit insurers are specifically looking at key areas of the outbreak to see whether they can reduce exposures to just a need basis only on their existing policyholders — what is being delivered, what is pending and what is being ordered.

During this time trade credit insurers are likely to reduce their cover to “need only,” yet insurance will cover “some insolvency or defaults on any valid due debt”. But one thing for sure is that the likelihood for accepting any new proposal at this time is typically zero.

On top of that, trade credit insurers have also given their policyholders’ and the buyers some flexibility to arrange payments and to deal with eventual delays by amending the policy with immediate effect, for example:

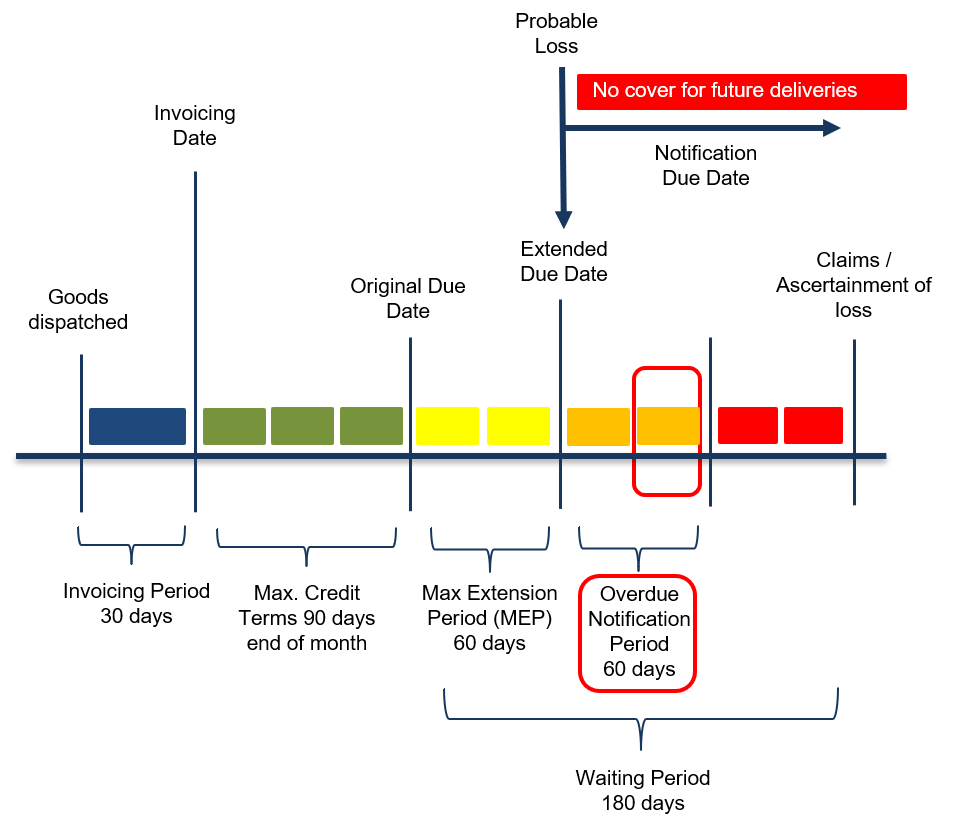

(a) To postpone the insured's obligation to notify a breach of the maximum extension period and/or insured's obligation to transfer collection cases with an additional 30 days. This period is now extended to 60 days.

(b) Insured is now allowed, WITHOUT approval to agree with their buyers / customers on a later payment for a receivable, even after the expiry of the maximum extension period, as long as these amended payment terms remain within the above mentioned 60 days after the expiry of the maximum extension period.

However, in the view of expert, businesses need to proactively manage their response and shift in mindset now from in preparation and planning mode to response mode. For instance, companies need to think about what happens if they lose a large proportion of their workforce, say 30%, which “could be the result of people getting sick themselves, self-quarantining, or because schools close and employees need to take care of kids at home.

CC Advisory will always be at your side and you can rely on us to provide you professional and clarity advice on business risk management which can often be a little challenging to understand.

Illustration: Upon the Pandemic crisis, Trade Credit insurer now covers policyholders on the protracted default of their buyers / customers with the maximum extension period and/or insured's obligation to transfer collection cases with an additional 30 days.

2. Easy Way to Manage Your Business Insurance

2.1 Buying Direct from Insurance Provider vs. Insurance Agent vs. Financial Advisor (FA)

There are so many ways and places for you as a business owner to get your business risk insurance. However, each of the channels will definitely bringing you different benefits, services and overall experiences. Let us tell you the difference of buying insurance directly from an insurance provider vs insurance agent vs FA. It should be a good guide for you to easily manage your business insurance.

2.1.1 Insurance Provider

Insurance provider is the organization or company that sells their in-house insurance products such as Allianz, Great Eastern, Prudential, AIA and a lot more in the market. If you are purchasing insurance directly from insurance provider, you will need to do a lot of research for their so-many-products before you decide on one which suitable for your company. Then you may proceed for quotation, buying, making payment and may have to do some amendment later to the policy. For all of this process involve, you have to deal and rely on the provider’s customer service call center.

The premium will be lower because you no need to pay for any intermediary fees. However, as a non-insurance-expert, do you know and are you confident enough that you are selecting the right product and sufficient coverage for your company insurance? For more options, you need to do your own comparison from different insurance providers. The downside is, after so much time spent with the whole process, you could end up with not having the right coverage or insufficient coverage.

2.1.2 Insurance Agent

Insurance agents are authorized to do business on behalf of an insurance company. An insurance agent may be authorized to solicit insurance business, collect premiums, and issue cover notes on behalf of the insurance company, depending on the terms of the agency agreement. Insurance agents will help you to understand the different insurance terms and coverage and help buyer at any time throughout the policy if have any issues, changes, or need to file a claim.

However, insurance agents would typically have a very limited number of plans available for you. So, they might push their very own company's products, which eventually may not provide you with the best and suitable products available in the whole insurance industry. Since there is not much options available, there is limited ways to do a yearly business risk insurance review for your company.

2.1.3 Financial Advisor (FA)

FA acting as a "one-stop-service-centre" by providing everything from portfolio management to insurance products. FA collaborates with variety of insurance companies to offers wide range of insurance products. FA will represent clients to select the most cost-effective insurance portfolio that matches their industry and needs. As a client to FA, you will be able to get the lowest premium and maximum benefits for you company business risk insurance. In term of the policy management, do not need to worry about the amendment, coverage, claim and etc where these will be managed well by your FA.

On top of it, FA not only provide insurance but will also assist your company to do cost saving, budget, tax strategies and sufficient coverage when the risk occur. FA will further check with clients on a regular basis to re-evaluate their current situation and future goals and plan accordingly. By engaging with FA, you are not only getting the business insurance services but also will get other value-added services such as financial advisory which will be very beneficial to your company or organization.

2.2 What Are The Smarts Ways To Claim Insurance?

(a) Make sure your claim approved using the right and efficient manner

On top of it, FA not only provide insurance but will also assist your company to do cost saving, budget, tax strategies and sufficient coverage when the risk occur. FA will further check with clients on a regular basis to re-evaluate their current situation and future goals and plan accordingly. By engaging with FA, you are not only getting the business insurance services but also will get other value-added services such as financial advisory which will be very beneficial to your company or organization.

When comes to claim, we will ensure the claim approved using the right manner. First of all, as a financial advisor, we will assist our clients to ensure the efficiency of claim process by understanding the insurance claim process and steps in order to avoid unnecessary steps.

However, when claims occurred, there are only 2 simple steps that you will need to follow in order to make the claim process more efficient. Firstly, you will need to notify us and report to police immediately when the claim occurred, following by providing necessary claim documents to us.

(b) Ensure the claim process is efficient and transparency

Should you appoint financial advisors rather than deal with insurance company directly? It depends on your opportunity cost of time. As a financial advisor, we are here to assist you to ease the claim process. We provide real-time updates of where their claim is in the process to our clients. Moreover, it saves the time for you to go through multiple steps to reach the experts or keep them waiting for a long time. We will assist you for the claim in a shorter period of time.

3. How To Save Cost From Your Existing Business Risk Insurance?

Cost can be one of the key decision factors when it comes to purchasing your business risk insurance. Thus, it is crucial to have a professional team or expert to assist you getting the optimum protection with lowest cost possible.

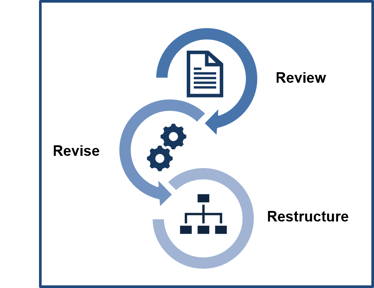

3.1 3R Strategy [ Save Insurance Cost ]

At CC Advisory, we are using a business risk insurance planning called 3R Strategy. It is our insurance analysis approach with the objectives of achieving cost saving and optimum insurance protection. This is the best way to reduce existing insurance cost for your company.

3.2 3R Strategy Framework

Our Financial Adviser Representatives (FAR) are working together with our competent Centre of Excellence (COE) team to review your existing insurance policies. Then, we source for the right insurance companies that match your company profile and industry to construct the best cost-effective insurance portfolio.

The steps taken during our 3R Strategy analysis are:

1. Review existing policy with historical claim report.

2. Revise existing insured protection, in order to achieve optimized protection

3. Restructure existing insurance in order to achieve 3R objectives either to lower cost or increase coverage.

Continue reading to understand each step in more details.

Sample of a 3R Strategy Report

Click Here to read more

4. Ease your Business Risk Insurance matter

At CC Advisory, client’s peace of mind is our top priority. We are here to ease your business insurance matter with our Centre of Excellence, COE team assistance. We offer independent insurance advisory services tailored-made to your needs with planning the objectives of achieving cost saving and optimum insurance protection. Our 3R Strategy is a holistic approach towards a more effective risk management.

4.1 General Service

CC Advisory’s COE is responsible for the top level of support for all business insurance clients. COE team are comprised of dedicated insurance specialists who will focus on the technical details as well as excellent client’s experience to ensure a smooth process and peace of mind for clients at all point of time.

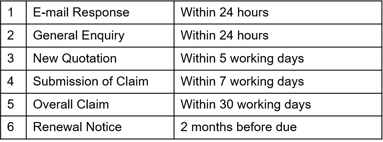

Below is the general service guideline by COE:

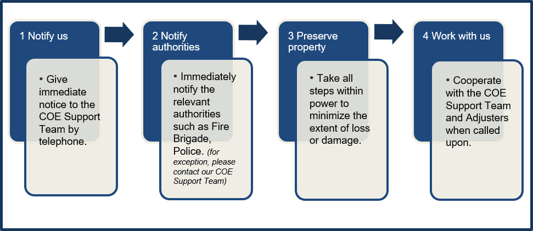

4.2 Claim Management

COE’s efficient claim management services will guide the client through the challenges of recovering from events and minimize the impact or risk to the business. COE’s objective is to ensure there will be no surprises within client’s expectations and claim can be settled within the most efficient time. COE’s claim services shall reduce cost and time for clients by utilizing the available technical know-how, market knowledge and relationships.

Below is the example of Fire Insurance Claim Process supported by COE team:

5. Successful Case Study

5.1 Case Study 1: How CC Advisory restructured the insurance program for one of Malaysia’s largest karaoke, hotel and F&B group

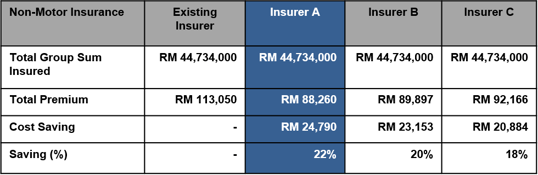

The client is a Malaysian family entertainment group with over 16 outlets nationwide. They were facing the cash flow challenges and pressures from lockdown during the tough MCO period due to the COVID-19 pandemic. The client was looking for all the possible solutions in order to lower down their operational expenses. Our experienced COE team got to work through insurance review for the client.

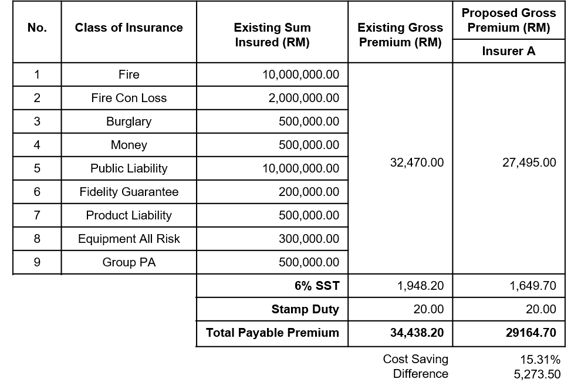

From the initial review and findings, it was identified that the client is having combined insured value of RM44mil with annual premium of RM113thousand. COE team was able to revise and restructure the insurance program of the client and successfully achieve a whopping 22% cost savings on the annual insurance premium.

COE team also worked diligently with the client to facilitate the restructuring of the insurance program on dealings with existing insurance company and bankers to ensure a smooth transition process. Through 3R Strategy, our team manage to provide client the conveniences & effectiveness on their business risk management portfolio.

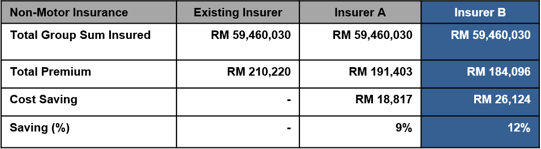

5.2 Case Study 2: CC Advisory providing added-values insurance coverage for a manufacturing company at no additional cost.

The client provides competitive manufacturing needs of a diversified range of OEM industries including aerospace, oil and gas, semiconductor and electronics. The client was seeking professional advice for their business risk management. Through our team experience dealing with various industry, we are able to evaluate and design a risk mitigation strategy for their business.

From the initial review, the client existing general insurance coverage is RM59mil in total portfolio with around RM210thousand of premium. After a thorough risk assessment process, our team manage to identify potential hazards and advise client to transfer potential risk exposure by proposing fire consequential loss & machinery breakdown insurance. Thus, by maintaining the group’s existing protection coverage, we manage to achieve cost saving up to 12% and also add value to their risk management portfolio.

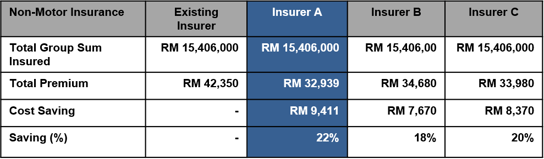

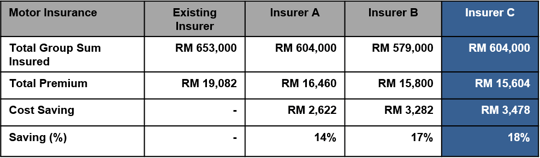

5.3 Case Study 3: Cost saving insurance program for a trading industry with Motor & Non-Motor insurance portfolio.

This food additives trading company has been paying over RM60thousand per annum over several years. Client finds our 3R strategy is beneficial to them to reduce the cost and have a review analysis of the total insurance portfolio as it was never done before.

Through 3R steps, we have managed to help client to achieve 22% cost saving for Non-Motor insurance while maintaining their current coverage and 18% cost saving for motor insurance. Client feels delighted that our 3R strategy able to help them to have better purchasing power. They are able to do a comparative analysis over short period of time and reduce their operation expenses concurrently with our COE team assistance.